Over the past three or so years, I have written well over 1,000 pages on personal finance and investing. Every…

Why the Stock Market Will Crash Soon

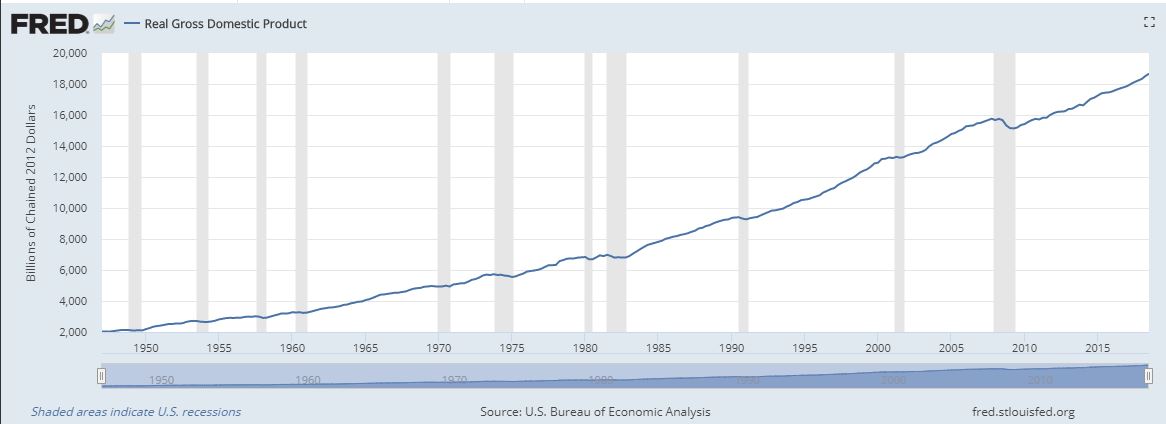

The Fed says that there will be more rate hikes than Wall Street expected, and market watchers yawned. Mr. Powell…

Professors in D&D (Episode 2021.8)

DM: As you will recall from our last adventure, the Crimson Cleric has risen to be the Supreme Leader of…

Black Swans in Social Scientific Inquiry

Nobel laureate Daniel Kahneman stated simply, “The Black Swan changed my view of how the world works” (Kahneman, 2011). On…

The AIs Have It: The Grim Future of Investing

In a recent Twitter thread started by the venerable Jim O’Shaughnessy (@jposhaughnessy), I said: If everyone were a rational long…

What does “Open” Mean in Open Educational Resource (OER)?

It may seem very strange to those not exposed to the Open Educational Resource (OER) movement, but the everyday term…

Demystifying Beta

It has often been said that “the market loves certainty.” Most investors (excluding those who seek to capitalize on volatility)…

Demystifying Market Corrections

When the market starts trending down, many investors tend to panic. They see volatility as dangerous and formulate a belief…

Demystifying Market Sectors

With all of the hoopla over various stock indices, it is sometimes easy to forget that the stock market is…

Demystifying Price Targets

One of the most important predictors of short-term stock prices is the backing of market analysts in the form of…

Demystifying the Financials Sector

Stock market analysts often worry about market volatility, which is jargon for a rapid cycling of upward and downward trends…

Demystifying the Oil and Gas Sector

As with most of the industries and sectors that stock investors may seek to invest in, the oil and gas…